Daily Nifty Analysis

|

| xDirect India's Nifty Analysis_26.06.2012 |

With the sudden drop in the market being witnessed yesterday, the government has announced today that it would take necessary steps to stem the Rupee depreciation; nevertheless these comments came in futile as global uncertainty has indeed gripped on the bull traders to resume on their trading with INR still hovering at its all-time low levels. For today we have a light on the counter from Euro Zone and UK, but US Consumer Confidence being the most important. However the Indian markets would trade sideways with supports coming in at interim levels of 5095 levels (Rising trend line). Followed by 5050 (50% retracement) and then 5023 (Falling trend line). Resistance is seen towards 5140, 5178 levels; however considering bearish trend has been commenced we believe Nifty has little chance of building momentum over 5180 levels for the week.

View on Indian Rupee

|

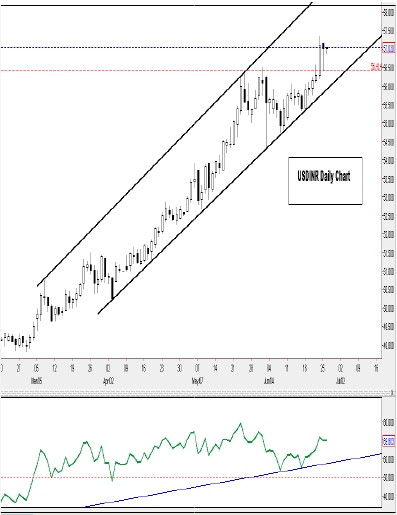

| xDirect India's USD/INR Analysis_26.06.2012 |

The main step announced was to increase in the cap on foreign investment in Indian government debt to $20 billion from $15 billion. The government also reduced the minimum period investors need to hold some bonds to three years from five years, making them more attractive to foreign funds.

The Indian Rupee is expected to trade in a tight spot where in, where on the upside the resistance is seen towards 57.42 (Fibonacci extension) followed by 57.65 levels. Supports come in at 56.40 (yesterday session low). There might be some sort of positives seen in the market considering the constant selling but we believe the bear trend would resume considering the ill-liquid FOMC state,, followed by the multiple downgrades. For today however we would want the US Consumer Confidence to give some amount of boost as yesterday’s housing sales marked good numbers, its best in 3 years.

For today the market is expected to be range bound however, where European session may mark some amount of swings in the global market which may give certain movement in the currency pair.